Newsletter: 176

Date: April 14, 2025

Economic analysis of Europe in the first months of the year:

The economic analysis of Europe in the first months of the year reveals a nuanced situation, with signs of recovery coexisting with persistent challenges. Here’s a detailed analysis backed up by key figures:

Note: U.S. tariff information has not been taken into account.

Economic growth:

- Gradual recovery:

- The European Commission has revised upwards its growth forecasts for the euro zone, anticipating growth of 0.8% in 2024 and 1.4% in 2025. This adjustment reflects greater resilience than expected at the start of the year.

- GDP increased by 0.4% MoM in January seasonally adjusted (December: +0.3% MoM), beating market expectations.

- Driving factors:

- Private consumption is strengthening, supported by a robust labor market and a gradual decline in inflation.

- Exports are also contributing to the recovery, although global uncertainty remains a limiting factor.

- Regional disparities:

- There are significant variations in growth between EU countries. For example, Spain is expected to experience growth of 2.1% in 2024, exceeding the Eurozone average.

Inflation:

- Gradual moderation:

- Inflation in the Eurozone has shown a downward trend, although it remains above the ECB’s 2% target.

- The European Commission now estimates that inflation will stand at 2.5% in 2024 and fall to 2.1% in 2025.

- Persistent pressures:

- Underlying inflationary pressures, such as labor costs and services prices, remain a concern.

- Geopolitical instability and energy prices may also generate new inflationary pressures.

Labour market:

- Fortress:

- The European labour market remains robust, with historically low unemployment rates.

- The unemployment rate in the Eurozone is expected to remain around 6.3% in 2025.

- Challenges:

- Labour shortages in certain sectors and the need to adapt to digitalisation pose structural challenges.

Risk Factors:

- Geopolitical uncertainty:

- The war in Ukraine and global geopolitical tensions remain the main source of uncertainty.

- Economic policies:

- The fiscal and monetary policies of countries and the ECB can have a significant impact on the economy.

- Energy prices:

- Energy price volatility remains a major risk to economic stability.

Key Sources:

- European Central Bank (ECB).

- European Commission.

- FocusEconomics.

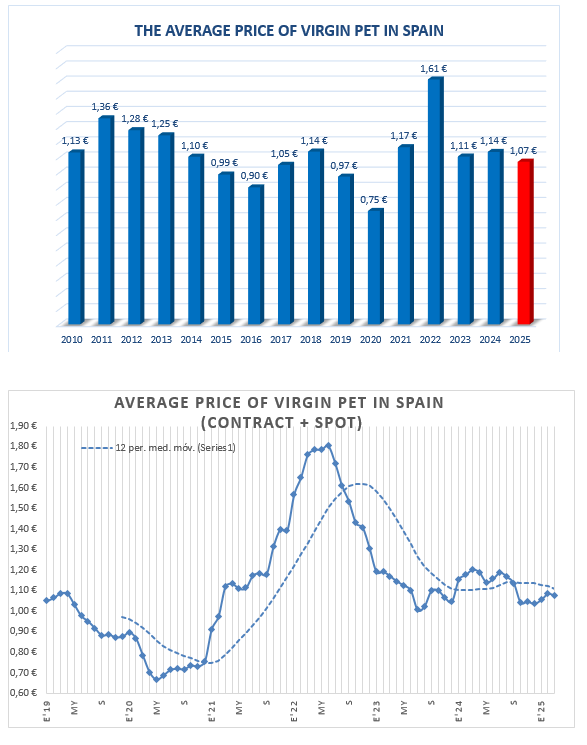

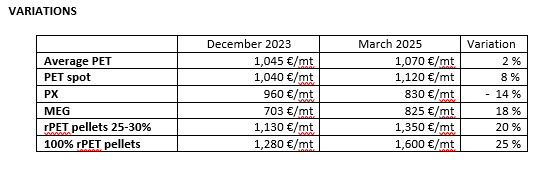

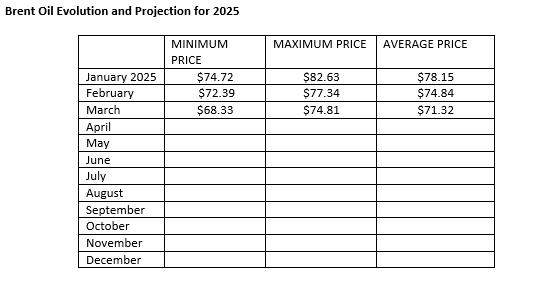

The PET market.

- Plastics Production in Europe:

- According to Plastics Europe:

- European plastics production in 2023 was 54 Mt, marking a decrease from 58.7 Mt in 2022.

- Fossil-based plastics in Europe were significantly reduced, from 47.2 Mt in 2022 to 42.9 Mt in 2023.

- Europe has gone from representing 14% of global polymer production in 2022 to 12.3% in 2023.

- This indicates a clear trend towards reducing the production of traditional plastics and a possible shift towards more sustainable materials, including rPET.

- According to Plastics Europe:

- PET Market Size:

- According to Mordor Intelligence:

- The size of the European polyethylene terephthalate market is estimated at $5.38 billion in 2024.

- It is expected to reach $7.17 billion by 2029, with a compound annual growth rate (CAGR) of 5.91% over the forecast period (2024-2029).

- Packaging is the sector with the highest participation within end users.

- Recycling and Waste:

- Information from the European Parliament:

- In 2021, the total plastic waste produced in the EU was 16.13 million tonnes.

- Approximately 6.56 million tons of plastic waste were recycled.

- This highlights the growing importance of recycling and waste management in the PET sector.

- Information from the European Parliament:

- Additional Data:

- The plastics industry in Europe employs more than 1.5 million people and is made up of more than 52,000 companies, according to Plastics Europe.

- An estimated 5.5 million tonnes of post-consumer recycled plastic were reintroduced into the EU27+3 economy in 2021, representing a significant increase compared to the previous year.

- According to Mordor Intelligence:

Important Considerations:

- The transition to the circular economy and EU regulations are transforming the PET market.

- The demand for rPET is on the rise, which influences production and consumption dynamics.

- Fluctuations in raw material and energy prices can affect production costs.

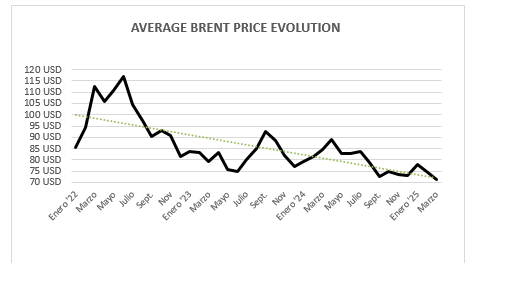

BRENT

The Brent oil market is in a reordering phase, with a number of factors converging to define a particular trend towards 2025. Here’s a detailed analysis, backed up by key figures:

Demand:

- Moderate growth:

- Global oil demand is expected to continue its ascent, albeit at a slower pace. Forecasts indicate an increase of approximately 1.1 million barrels per day (b/d) in 2025.

- This growth is influenced by the moderation in the growth of the main consuming economies:

- United States: Growth is forecast at 2.0% (compared to 2.7% in 2024).

- China: Growth is estimated at 4.1% (up from 4.8% in 2024).

- Eurozone: growth of 1.0% is anticipated (from 0.8% in 2024).

- Energy transition:

- The adoption of electric vehicles and increasing investment in renewables are starting to impact demand in the long term, although their effect in 2025 will be relatively limited.

Offer:

- Non-OPEC+ production increase:

- A significant increase in non-OPEC+ production is forecast, with an estimated increase of 1.4 million b/d in 2025.

- The United States is leading this growth, although shale production could be affected by lower prices.

- Production from Latin American countries, such as Brazil, and Guyana is increasing, causing greater supply.

- OPEC+ decisions:

- OPEC+ has implemented production cuts to support prices, and its strategy in 2025 will be crucial.

- The organization is planning to increase its production gradually, but this measure is subject to change depending on market conditions.

Prices:

- Downward trend:

- A downtrend in Brent prices is anticipated, with an expected average of around $73 per barrel in 2025.

- This decline is due to the increase in supply and the moderation in demand growth.

- Volatility:

- Geopolitical events, such as tensions in the Middle East, and OPEC+ decisions could lead to significant fluctuations in prices.

- Analysts at Goldman Sachs forecast that Brent crude will average $76.00 per barrel. J.P. Morgan takes a more bearish stance, projecting Brent at $73.00 per barrel.

Key factors:

- Global economic growth: The evolution of the world economy, especially in China and the United States, will be decisive for demand.

- OPEC+ decisions: OPEC+ production policies will have a significant impact on supply and prices.

- Non-OPEC+ production: Increased production in countries such as the United States and Brazil will partly balance OPEC+ cuts.

- Energy transition: In the long term, the transition to cleaner energy will influence oil demand.

- Geopolitics: Geopolitical conflicts and tensions cause great instability in prices.

Sources of information:

- BBVA Research

- International Energy Agency (IEA)

- Goldman Sachs.

- J.P. Morgan.

It is essential to consider that these forecasts are subject to change, and the evolution of the oil market may be altered by various unforeseen factors.

GDPR: Data Protection Information of MARSELLÀ GLOBAL S.L. (smarsella@marsellaglobal.com):

PURPOSE: To inform you of our products and services by electronic means. LEGITIMATION: Legitimate interest in keeping you informed in your capacity as a client and/or user. ASSIGNMENTS: Not contemplated. CONSERVATION: During the contractual relationship and/or until you request us to cancel the contract and during the periods required by law to meet any liabilities once the relationship has ended. RIGHTS: You can exercise your right of access, rectification, deletion, portability of your data and limitation or opposition in the email of the responsible party. In the event of disagreements, you can file a complaint with the 72Data Protection Agency (www.aepd.es).

This newsletter is prepared based on the information and experience of our sales team. Marsella Global, SL pays special attention to its preparation, however, we cannot guarantee the accuracy and usefulness of the content published.

The recipient accepts the content of this newsletter on the understanding that Marseille Global, SL is not responsible for any damage caused by the use of the information contained in this document.

Comments are closed.