Newsletter: 182

Date: February 18, 2025

PET 2025

Size and Structure of the PET Market in Europe (2025)

- Europe accounted for approximately 25-26% of the global PET market.

- Estimated European market value: USD ≈15.1 billion in 2025.

- Dominant application: food and beverage packaging (~82%).

The main markets (EU-5: Germany, France, Italy, Spain and the UK) are mature and value-oriented, with strong pressure towards sustainability and recycled content.

Europe is not growing as much in volume as Asia, but it is growing in added value, regulation and recycling.

Demand in 2025: behaviour by sector

Beverage containers (main driver)

- It continued to be the largest consumer of PET.

- The material remained competitive against aluminum and glass due to:

- Logistics

- Total cost

- Lightness

However, “anti-plastic” sentiment in some markets led to tests with alternatives (aluminum), although without significant structural impact.

Trays & Thermoforming

- Growth due to the substitution of PS, PP and EPS in retail.

- Driven by recyclability and ESG goals.

Conclusion: 2025 was a year of stable demand with moderate growth, but with a shift towards recyclable applications.

European Key Factor: rPET Explosion

Europe was the market most influenced by recycling in 2025.

Main reasons:

- EU target: 25% recycled content in bottles by 2025.

- Single-use plastics directive.

- Extended producer responsibility (EPR) regulations.

Europe leads the global rPET bottle market thanks to:

- Deposit systems (DRS) with >90% return rates in countries such as Germany and the Nordics.

- Advanced recycling infrastructure.

The European rPET market:

- ≈3.86 trillion USD in 2025

- Expected CAGR 7.8% through 2032.

Important Insight:

In Europe, PET is no longer just a petrochemical polymer — it is part of the regulated circular economy.

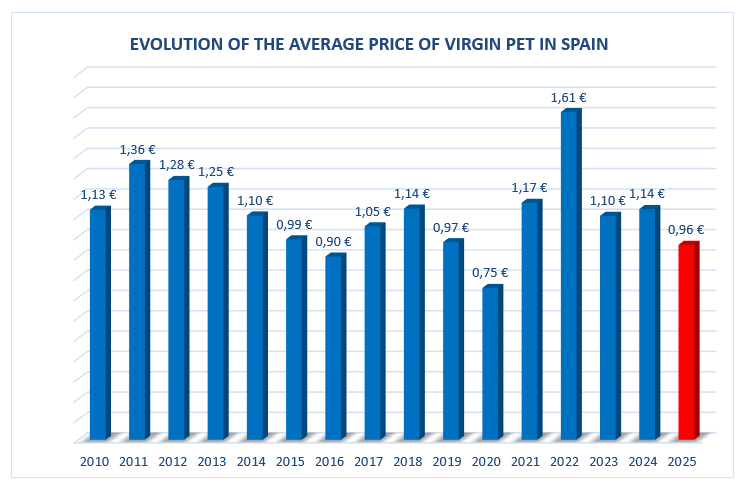

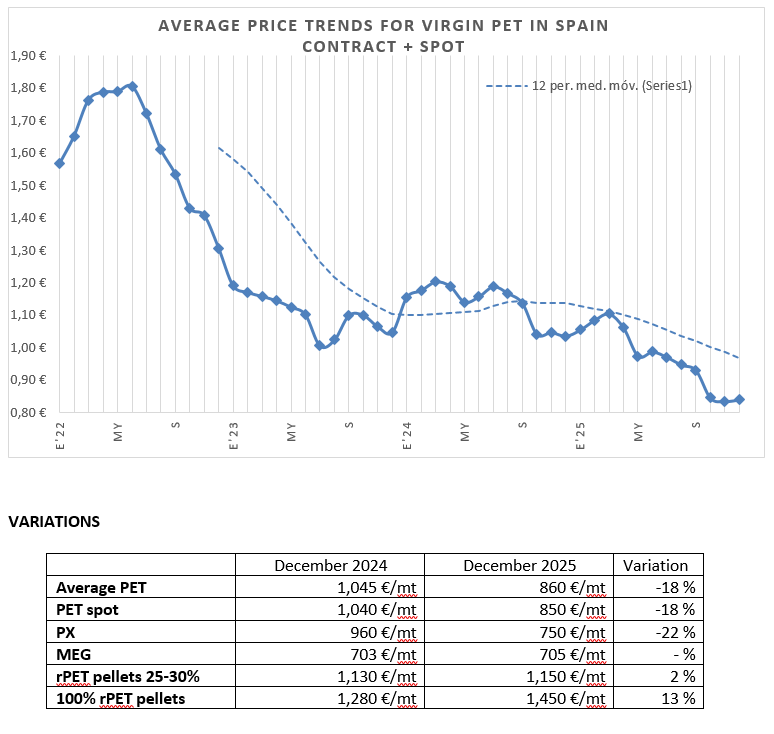

Price developments in Europe in 2025

Typical PET bottle range in 2025:

- Approximately €1,130–1,170/t

Bearish factors

- Lower raw material costs (PTA/MEG) vs 2024.

- Global oversupply (especially Asia).

- Competitive imports.

Bullish factors

- Expensive energy in Europe.

- Production stoppages.

- Anti-dumping measures.

- Regulatory costs.

A relevant phenomenon was the partial disconnect between oil and PET due to trade policies and tariffs.

2025 was a year of relatively contained prices but artificially sustained by European regulation and energy costs.

Industrial supply and competitiveness

Structural problems in Europe:

- High energy costs compared to Asia and the Middle East.

- Competition from cheap imports.

- Regulatory pressure.

In fact, the European recycling sector lost capacity in 2025 due to:

- Low prices of imported virgin PET.

- High energy costs.

This led to:

- New EU trade measures.

- Anti-dumping against Chinese PET.

- Preparation of stricter controls on imports.

Structural risk: loss of European industrial competitiveness.

Regulation: the great conditioning factor of the European market

Europe is the region where regulation has the greatest impact on PET.

Key elements in 2025:

- Mandatory recycled content targets.

- Packaging taxes in some countries.

- Expanding mandatory deposit systems.

- Upcoming PPWR (Packaging and Packaging Waste Regulation) regulation.

In addition:

- The EU is considering import controls to protect local recyclers.

The European market is moving from being price-driven to policy-driven.

Overview of the European PET market in 2025

Positives

Stable demand in beverages

Global Leadership in Recycling

Innovation in circularity

High added value

Negatives

High energy costs

Asian import competition

Growing regulatory pressure

Limited industrial profitability

Structural trends that became clear in 2025

The most important trends:

- rPET will be the main growth driver in Europe.

- Regulation will set prices and demand more than oil.

- Possible industrial consolidation (closures or mergers).

- Greater European trade protection.

- Differentiation between integrated and non-integrated producers.

Post-2025 Overview

The European market is entering a phase of:

transition to a regulated circular model with global competitive pressure

This involves:

- Virgin PET with limited growth.

- rPET with strong growth.

- Volatility due to regulation.

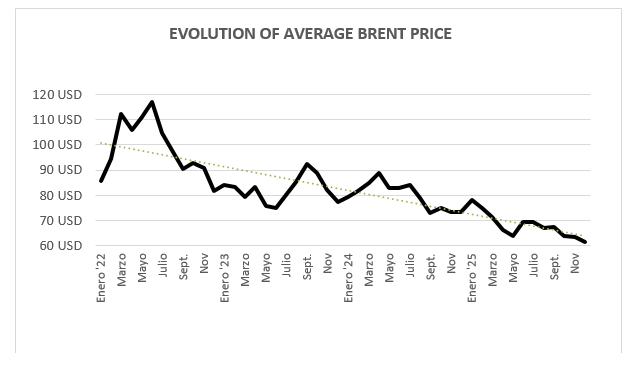

BRENT

The performance of Brent crude oil has been marked by a transition from geopolitical volatility to a scenario of structural oversupply.

2025 Analysis: The Year of the Correction

2025 was a year of diminishing returns for Brent, driven by weaker-than-expected global demand and rising production.

The year started strongly at 82-83 USD, but closed December at levels of 63 USD, its lowest monthly average since 2021.

Despite OPEC+’s efforts to contain production, growth in non-OPEC countries (notably the US, Brazil, and Guyana) led to excess inventories. Production is estimated to have exceeded consumption by more than 2.5 million barrels per day in the second half of the year.

Economic weakness in China and its aggressive transition to electric vehicles slowed demand growth. Only strategic purchases for its reserves prevented the price from falling below $60 early.

Although tensions in the Middle East and Ukraine caused temporary spikes (such as the jump to $85 in April), the market ended up prioritizing supply and demand fundamentals over political risk.

2026 Outlook: Towards a $50 floor?

For 2026, the consensus of the main bodies (EIA, Goldman Sachs, J.P. Morgan) points to an even more downward pressure market.

Price Projections

| Institution | Average Brent Price 2026 |

| EIA | ~58 USD |

| Goldman Sachs | ~56 USD |

| J.P. Morgan | ~54 USD |

| ABN Amro | ~$55 (down to $50 by year-end) |

Key Factors for this year

- Inventory Glut: The EIA forecasts that production will continue to outpace demand, maintaining steady downward pressure. OECD commercial inventories are expected to reach critical storage levels.

- OPEC+ at the crossroads: The group faces the dilemma of continuing to cut production (losing market share) or allowing prices to fall to force out producers with higher costs (such as U.S. shale).

- Geopolitical Resilience: At the beginning of 2026, occasional tensions with Iran and purchases by India have kept Brent oscillating between 65 and 70 USD, but analysts consider them to be technical rebounds in a long-term bearish structure.

- Technical Levels:

- Critical Support: 55 USD. If broken, the next target is $49-50, a level where U.S. shale production starts to become unprofitable.

- Resistance: $62.60 and $68. Breaking above $70 on a sustained basis would require a massive supply shock or a radical shift in the Chinese economy.

Summary: 2026 is shaping up to be a year of “low prices to rebalance the market”. Barring a conflict that physically disrupts the flow of crude, the path of least resistance for Brent remains sideways-bearish.

Brent Oil Evolution for 2025 (USD)

| MINIMUM PRICE | MAXIMUM PRICE | AVERAGE PRICE | |

| January 2025 | 74,72 | 82,63 | 78,15 |

| February | 72,39 | 77,34 | 74,84 |

| March | 68,33 | 74,81 | 71,32 |

| April | 58,40 | 74,47 | 66,32 |

| May | 58,50 | 66,81 | 63,70 |

| June | 63,00 | 79,40 | 69.39 |

| July | 66,34 | 73,63 | 69,42 |

| August | 64,79 | 72,00 | 67,13 |

| September | 65,07 | 70,76 | 67,52 |

| October | 59.97 | 66,64 | 63,86 |

| November | 61,26 | 65,32 | 63,52 |

| December | 57,72 | 64,09 | 61,56 |

GDPR: Data Protection Information of MARSELLÀ GLOBAL S.L. (smarsella@marsellaglobal.com):

PURPOSE: To inform you of our products and services by electronic means. LEGITIMATION: Legitimate interest in keeping you informed in your capacity as a client and/or user. ASSIGNMENTS: Not contemplated. CONSERVATION: During the contractual relationship and/or until you request us to cancel the contract and during the periods required by law to meet any liabilities once the relationship has ended. RIGHTS: You can exercise your right of access, rectification, deletion, portability of your data and limitation or opposition in the email of the responsible party. In the event of disagreements, you can file a complaint with the 72Data Protection Agency (www.aepd.es).

This newsletter is prepared based on the information and experience of our sales team. Marsella Global, SL pays special attention to its preparation, however, we cannot guarantee the accuracy and usefulness of the content published.

The recipient accepts the content of this newsletter on the understanding that Marseille Global, SL is not responsible for any damage caused by the use of the information contained in this document.

Comments are closed.